Ever since the 1970s, the U.S. Federal Reserve has operated under a dual mandate that remains central to policy today: to maximize employment while stabilizing prices and maintaining long-term interest rates at sustainable levels.

Maximizing employment means keeping job levels consistent with “normal” economic conditions, instead of levels seen during overheated or recessionary economies. Meanwhile, price stability is also crucial for consumers and businesses to have confidence in predictable economic conditions to make long-term plans.

With that in mind, it can be understandable why investors follow every Fed interest rate decision and the press conference that follows after conducted by Fed Chair Jerome Powell.

Going into the Federal Reserve’s interest rate decision on Wednesday, September 17, it is looking more than likely that the Fed will cut rates on data suggesting a weakening U.S. labor market.

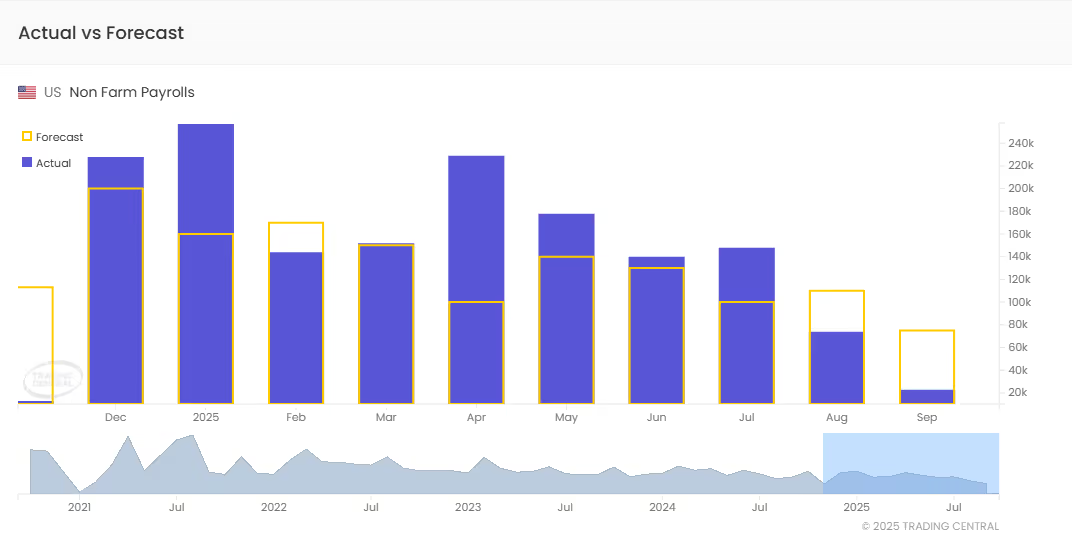

Recent data releases in September have painted a gloomy picture. Non-farm payrolls dropped to 22,000 in August, significantly lower than the expected 75,000 and the revised 79,000 for. The unemployment rate rose to 4.3%, surpassing the anticipated 4.2% and matching July's number. Meanwhile, ADP Employment reported a rise of 54,000 jobs in August, falling short of the expected 65,000 and considerably lower than the 104,000 recorded in July.

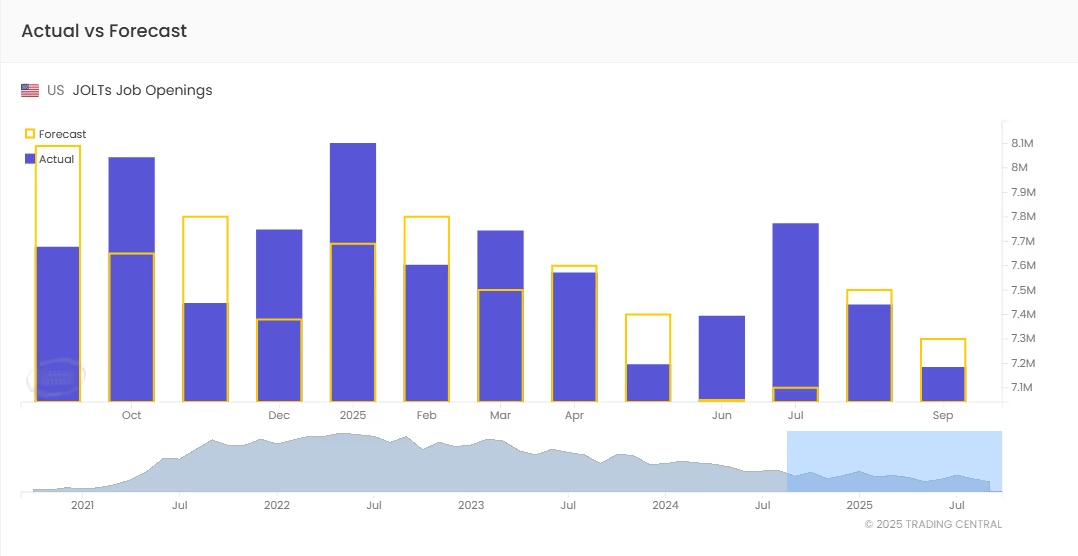

Moreover, the JOLTs report showed job openings decreased to 7.18 million in July, falling short of the anticipated 7.3 million. This marks the first instance since April 2021 where the number of unemployed individuals in the U.S. exceeded the available job openings.

Perhaps most concerning was the annual benchmark revision to nonfarm payrolls, which revealed a downward adjustment of 911,000 jobs for the year through March 2025. This sizable revision highlights that job growth in prior reports was significantly overstated, raising fresh doubts about the underlying strength of the labor market.

Prior to all these updates, in his address at Jackson Hole on Friday, August 22, Fed Chair Jerome Powell suggested that a weakening U.S. labor market may require an "adjustment" to the Federal Reserve's policy stance. His comments hinted at a growing willingness to ease monetary conditions, and with the accumulation of weaker data since then, the probability of a September rate cut has risen considerably.

The Fed has also been balancing concerns about elevated inflation, compounded by uncertainty around tariffs imposed by the Trump administration. These tariffs raise costs for producers and consumers while adding unpredictability to future inflation trends and business making.

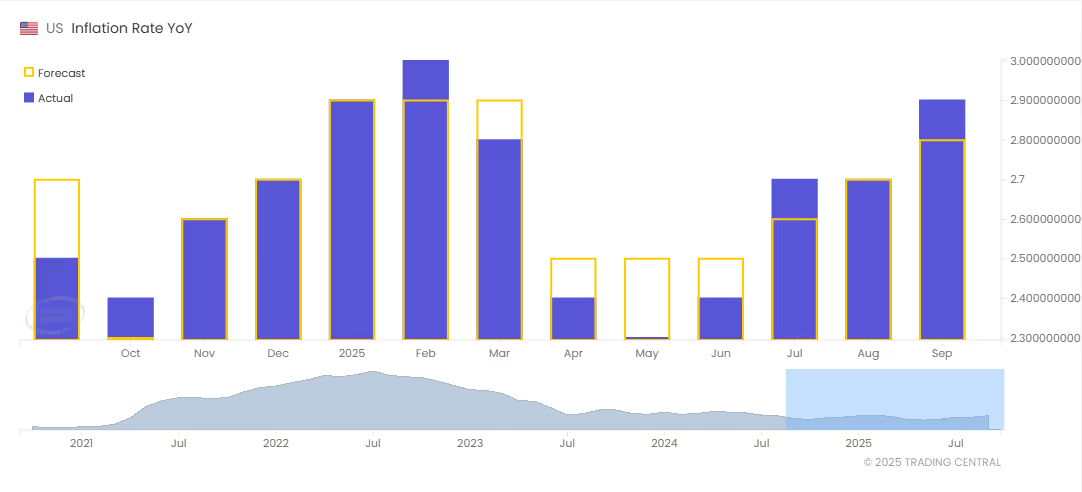

Recent inflation data has been mixed. The inflation rate for August was reported at 2.9% year over year, exceeding the expected 2.8% and rising from 2.7% in July. On a month-to-month basis, it increased by 0.4%, surpassing the anticipated 0.3%. In addition, the core inflation rate also rose to 3.1% year over year in August, aligning with expectations, while month-over-month core inflation increased by 0.3%, as anticipated.

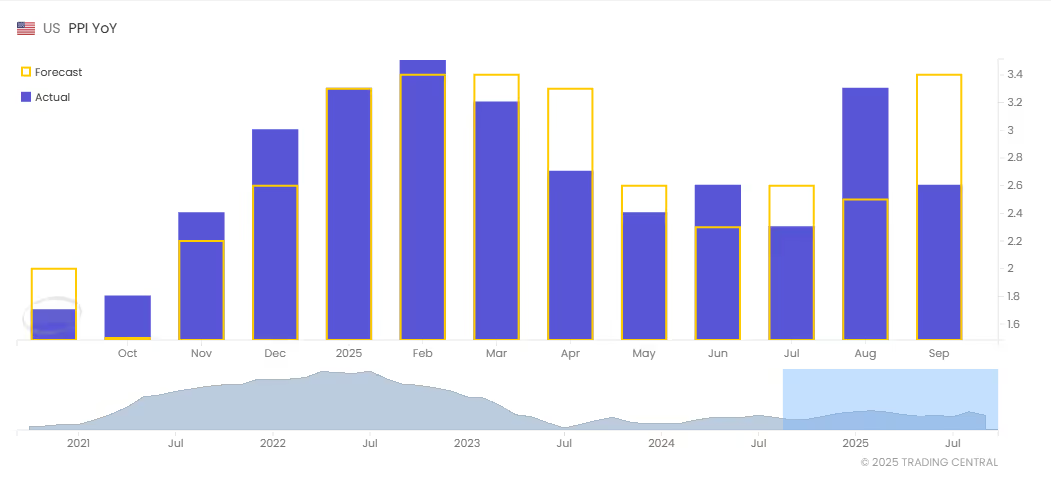

Meanwhile, the Producer Price Index (PPI) decreased to 2.6% year-over-year in August, compared to the anticipated rise of 3.4% and the 3.1% reported for July (which was revised from 3.3%). On a month-over-month basis, the index fell by 0.1%, while a 0.4% increase had been expected. The PPI, which measures price changes that producers receive for goods and services, is often seen as an early signal of inflation trends. Tariffs can push PPI higher by raising costs for producers, which may eventually filter through to consumer prices.

Powell has been adamant about tariffs creating an unpredictable path for future inflation. However, the latest inflation data has been received with mostly neutral reactions, suggesting investor sentiment favoring a rate cut.

According to the CME FedWatch, there is a 96% probability that the Fed cuts its benchmark interest rate to a range of 4.00-4.25%, with a 4% of a larger cut to a range of 3.75-4.00%.

In the days and weeks following the September 17 decision, several key releases will provide further clarity on the economic outlook:

While the Fed’s dual mandate focuses on employment and price stability, a broader set of indicators helps understand the overall economic picture. Investors are recommended to monitor manufacturing and housing data, while also keeping an eye on consumer confidence data.

As new data emerge, the Fed’s path forward could shift considerably. Weakness may warrant further rate cuts, while resilience could argue for a pause - or even a return to tightening should inflationary pressures resurface. Whatever the case may be, make sure to keep up to date with the latest economic developments in the U.S., or any country you are interested in, using Trading Central’s Economic Insight.

.png)

.png)

.png)